Why should employers care about their experience modification (e-mod) factor? Without knowing it, some employers are being overcharged for workers’ compensation premium year after year. They have the misconception that the e-mod is out of their control, but the fact is that they can take steps to improve this factor and reduce costs.

Since e-mod is an indicator of an employers’ workers’ compensation loss history compared to its industry peers’, it’s used as a multiplier to increase or decrease premium.

Well-informed employers will obtain an annual review of the data used in their e-mod calculation and the actual promulgation of their e-mod. Equally valuable is a more comprehensive analysis that focuses on the controllable mod and the losses driving current costs. For some organizations, these opportunities can reduce premium by 5% to 15% in the first year and create potential future savings upwards of 30%.

Results like this not only can improve the overall financial health of an organization, but also increase its growth and profitability, as a lower e-mod improves the organization’s ability to bid on and win new contracts and projects.

Employers can take these crucial steps toward improving their e-mods and workers’ compensation programs:

1. Understand the E-Mod Factor and How It Impacts Premium

Many employers believe they can’t lower their e-mod because they (or their insurance agents) don’t understand how the factor works. E-mod is a component of workers’ compensation pricing models used by insurance companies and has a direct impact on premium.

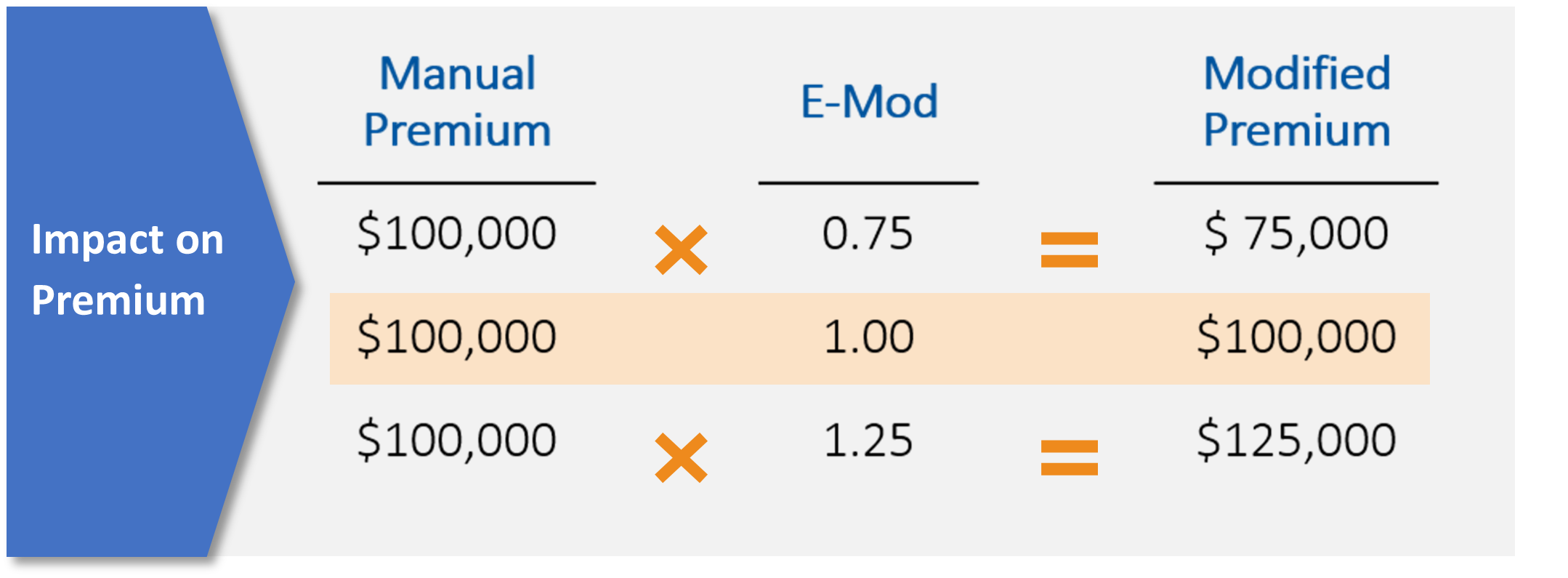

The e-mod is a measure of how your workers’ compensation loss experience compares to your peers’ — the calculation compares actual losses to “expected losses” of your peer group. The industry average is always expressed as an e-mod of 1.00, which doesn’t change the manual premium (the starting point for all calculations in the rating algorithm), as you can see in the chart above.

As the chart demonstrates, your e-mod has a direct correlation to the premiums you pay. As your e-mod improves or worsens as compared to the industry average, there’s a corresponding impact to your workers’ compensation costs. An e-mod of 1.25 leads to a 25% increase in premium, while an e-mod of 0.75 results in a 25% reduction in premium. Just as significantly, many large projects and government contracts require companies to have an experience modification rate of no more than 1.00.

2. Analyze Your Current E-Mod to Confirm Accuracy and Correct Errors in Premium

Because promulgation of the e-mod is complex, the process often results in errors and inflated premium. E-mods are calculated using losses and audited payrolls that are reported by the insurer to the states’ rating bureaus or advisory boards. Errors in the data used to promulgate the e-mod and the actual calculation of your e-mod can occur, impacting the e-mod and the amount of premium that you must pay. These key factors drive the calculation:

- Job classification — Are your class codes accurate? Changes in operations, staff and job responsibilities can result in miscoding errors and overpayment of workers’ compensation premium.

- Payroll — This may be erroneously overstated (e.g., overtime and bonus payroll, or certain portions of executive compensation).

- Claims — Are claims and reserves accurate? E-mod is calculated based on the last three years of claim history.

An error in any one of these areas can result in overpayment of premium. An effective analysis will review all data used to calculate the e-mod, correcting errors and ensuring that premiums reflect e-mod improvement.

3. Quantify Future E-Mod Improvement and Premium Savings

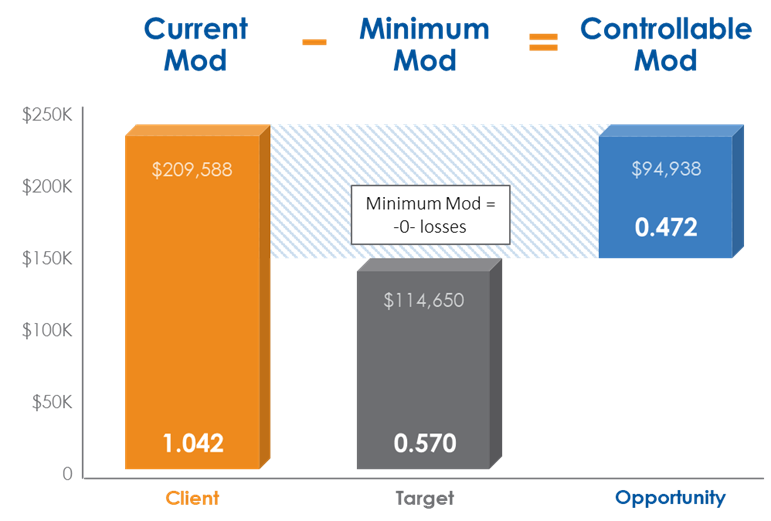

Following a review and confirmation of your e-mod’s accuracy, a more comprehensive analysis is critical for quantifying your future opportunity to further improve your e-mod. The analysis pivots from a retrospective review to a prospective analysis of your controllable e-mod, and to the future saving opportunity if you were to continue to drive down your e-mod.

The controllable mod is the difference between the current mod and the minimum mod. These values are important because they highlight the savings that are possible by controlling losses with targeted risk management strategies.

4. Analyze Claims and Identify Loss Trends Driving Your Current E-Mod

Once the controllable mod is established, a detailed claims analysis will determine which claims and trends are driving the current e-mod and preventing continued savings. The analysis should focus on historical loss trends, such as the nature, cause and location of losses, with attention given to the impact these losses have on your experience modification factor and resulting workers’ compensation premium.

Recent Posts

The “Hidden Pay Raise” Your Broker Forgot to Mention

It happens every year. Your renewal notice arrives with a double-digit increase, and your broker, who probably hasn’t been seen since last year’s enrollment, gives [...]

Safety on the Road: Are Your Adverse Weather Plans Ready?

Driving for work is a high-stakes responsibility, but when the forecast turns sour, the danger spikes significantly. Recent data shows that weather plays a role [...]

Is Your Shop Truly Safe? The Essential Guide to ALI Lift Inspections

Your automotive lifts are the literal backbone of your garage, hoisting thousands of pounds day after day. Because they are such reliable workhorses, it’s easy [...]