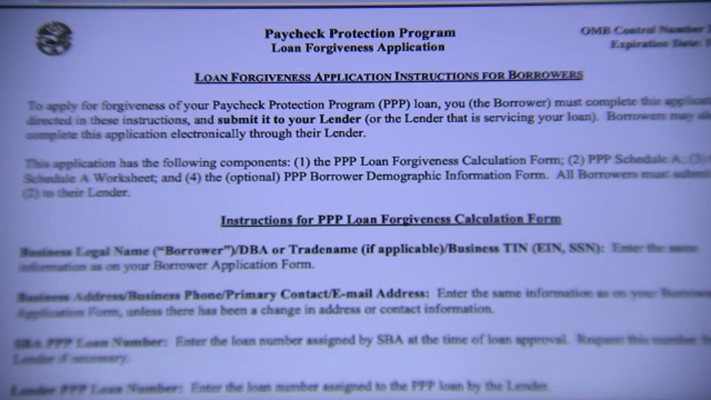

The Treasury Department and the U.S. Small Business Administration (SBA) just released the Paycheck Protection Program (“PPP”) Loan Forgiveness Application. The accompanying instructions and worksheets are very helpful in explaining how employers who borrowed PPP money can obtain forgiveness of their loans. Here are some highlights:

- Average Full-Time Equivalent Employees: Average full-time equivalent employees are based on a 40-hour workweek. Employers should enter the average number of hours paid per week for each employee, divide by 40, and round to the nearest tenth. The maximum for each employee will be capped at 1.0. The instructions also offer a simplified method that assigns a full-time equivalent number (FTE) of 1.0 for employees who work 40 hours or more per week and 0.5 for employees who work fewer hours, at the employer’s option. This is important for purposes of computing any reductions to the loan forgiveness amount based on headcount. Be consistent in computing full-time equivalent numbers for each measured period.

- Excused Reductions in Workforce: Employers who laid off employees (between February 15, 2020 and April 26, 2020) and offered to rehire the same employee, but whose employees reject such offer of re-employment, will not be penalized if the employer made a good faith, written offer of rehire, and the employee’s rejection of the offer is documented. In addition, the forgiveness amount will not be reduced for (i) termination of an employee for cause, (ii) voluntary resignation by employee, or (ii) a reduction of hours at the voluntary request by an employee.

- Eligible Forgiveness Costs: Payroll costs eligible for forgiveness include: (a) incurred payroll costs: Payroll costs are incurred on the day that the employee’s pay is earned; (b) Paid payroll costs: Payroll costs are paid on the day that paychecks are distributed or when the employer initiates an ACH credit transaction. Payroll costs for which forgiveness is sought must be paid during the 8-week forgiveness period, except that payroll costs incurred but not paid during the employer’s last pay period of the 8-week forgiveness period (or alternate covered period*) are eligible for forgiveness if paid on or before the next regular payroll date. Employers may elect an alternate payroll covered period, which allows them to begin the eight week pay period on the date that begins on the first day of their first pay period following the disbursement date of the Paycheck Protection Program loan, for administrative convenience. This applies only for payroll costs, not rent, utilities, and interest on mortgage obligations. Eligible nonpayroll costs must be paid during the 8-week forgiveness period or incurred during the 8-week forgiveness period and paid on or before the next regular billing date, even if the billing date is after the 8-week forgiveness period. Please be reminded that eligible nonpayroll costs, i.e. qualifying rent, mortgage interest and utilities, may not exceed 25% of the forgiveness amount (or the PPP loan amount).

Please be sure to contact us if you need any assistance or have additional questions concerning the loan forgiveness application. In the meantime, please click here for a copy of the application.

Recent Posts

The U.S. Department of Labor Announces Proposed Rule To Protect Indoor, Outdoor Workers From Extreme Heat

The U.S. Department of Labor has proposed a new rule aimed at protecting workers from extreme heat hazards. This initiative seeks to safeguard approximately 36 [...]

Supreme Court Overturns Chevron Deference: What It Means for Workplace Safety and Regulation

The landscape of federal regulation is set for a seismic shift following a recent Supreme Court decision. On June 28, in Loper Bright Enterprises, et [...]

Navigating the Compliance Maze: How NARFA Simplifies Employee Benefits for Automotive and Trade Industries

In today's complex regulatory environment, businesses in the automotive, roads, fuel, and related industries face unprecedented challenges in managing employee benefits. Recent studies show that [...]